Floating Above the Rest

31-Dec-24ETF Stream

14-Jan-25Floating Above the Rest

31-Dec-24ETF Stream

14-Jan-25Insights

CLO markets and ETFs

Miguel Ramos Fuentenebro

Co-founder and Partner

Understanding the distinction between public and private market access

As traditional portfolio construction evolves and asset managers expand their private market offerings, investors face important questions about accessing institutional markets. Recent Financial Times coverage highlighted a broader debate about retail participation in traditionally institutional assets. Within this discussion, it's crucial to understand why CLO ETFs represent a fundamentally different proposition from retail access to private markets. This analysis examines the structural differences, supported by historical data on market functioning, liquidity mechanisms, and risk characteristics.

Understanding market structure: CLOs vs private assets

The fundamental distinction between CLO markets and private assets lies in their trading infrastructure and price discovery mechanisms:

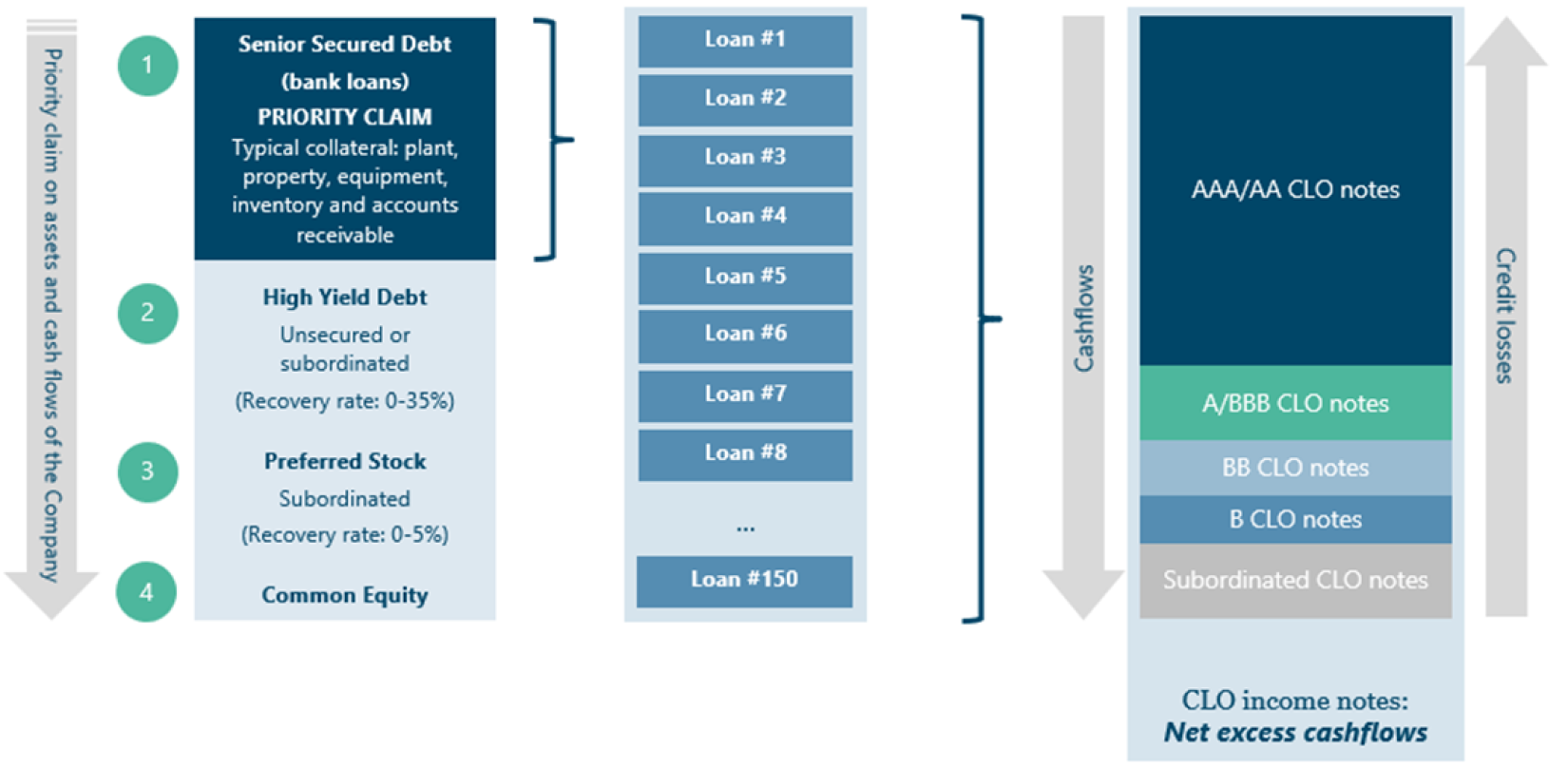

CLO markets

The CLO market, with $1.24 trillion in total size across the US ($974bn) and Europe ($266bn), represents an established, public market that has served institutional investors for decades.1

The CLO market operates through two complementary channels that create robust liquidity. The primary channel is the BWIC (Bid Wanted in Competition) process, which handles approximately 60% of trading volume.2 This unique mechanism demonstrates several key features of public market trading:

-

- Transparent price discovery: All market participants receive BWIC information, including price levels and trading outcomes, creating a continuous flow of market data.

- Standardised settlement: Trades settle on a T+1/T+2 basis, identical to traditional bond markets, enabling efficient portfolio management.

- Crisis resilience: During March 2020's market stress, BWIC volumes reached record levels ($7.7bn in US markets), showing the market's ability to function during volatility.3

Private markets

In contrast, private markets operate with fundamentally different characteristics:

-

- Limited price discovery: Valuations typically occur quarterly, with minimal public transaction data.

- Extended settlement: Trades can take weeks or months to complete, involving complex documentation and transfer processes.

- Restricted access: Investments often require long lock-up periods and high minimum commitments.

Glossary of CLO trading terms

BWIC (Bid Wanted in Competition)

An investor-to-investor auction used to trade a significant percentage of CLO notes on a daily basis via a listing and bidding process.

T + 1 / T + 2 settlement period

The time it takes to finalise a trade (exchange the security and payment) after the trade date (T). CLO secondary market trades generally settle in the same cycle and other assets such as bonds - 1 business day post trade date in the US and 2 business days post trade date in Europe.

ETF structure alignment

The success of CLO ETFs, exemplified by products like JAAA ($16.5bn AUM), stems from the natural alignment between ETF structures and CLO market characteristics. ETFs require:

-

- Reliable daily pricing: Limited price discovery: CLO markets provide continuous price discovery through dealer quotations and BWIC activity.

- Efficient creation/redemption: The established T+1/T+2 settlement cycle supports smooth ETF operations.

- Market depth: Average monthly trading volumes of c.€3.5 billion in EU-compliant CLOs support ETF scaling.4

Risk profile and historical volatility

The stability of CLO markets is demonstrated not just through diverse institutional participation but through concrete volatility metrics. Over the past five years - a period that includes significant market stress events like the 2020 pandemic shock and 2022's rate volatility – AAA-rated European CLOs have exhibited remarkably low volatility of 2.5%, comparable to German 2-year Bunds (1.7%). This stability is particularly noteworthy when compared to AA-rated corporate bonds, which have experienced volatility of 3.0% over the same period.5

This remarkable stability through market stress periods can be attributed to the strong fundamental performance (no AAA-rated CLO has ever defaulted) and to several structural characteristics that distinguish CLO markets from other fixed income sectors:

First, CLOs are floating-rate instruments, meaning their coupons adjust with changes in base rates. This feature results in minimal interest rate duration, protecting investors from the type of price volatility that fixed-rate bonds experience when interest rates change. During 2022's sharp rate increases, this floating-rate nature proved particularly valuable.

Second, the CLO market's institutional investor base contributes significantly to its stability. Banks, insurers, and pension funds typically employ long-term investment strategies driven by liability matching and income generation rather than short-term trading. This patient capital approach means these investors are less likely to engage in reactive buying or selling during market stress, helping maintain price stability.

Third, and perhaps most importantly, CLOs offer genuine portfolio diversification precisely because they have not become an overcrowded trade. Unlike some markets where oversupply of capital can amplify market movements, CLO ownership remains concentrated among sophisticated institutional investors who understand the asset class in depth. This specialized investor base helps maintain market discipline.

The AAA CLO market further benefits from diverse institutional participation that enhances these stability factors with banks (29%) and insurers (26%) providing stable long-term capital.6

Portfolio applications

For investors reconsidering traditional allocations, CLO ETFs offer several advantages:

-

- Floating rate exposure: Natural hedge against rising rates.

- Credit risk: No AAA-rated CLO has ever defaulted.

- Yield enhancement: Potential spread pickup versus similarly rated corporate bonds.

- Low volatility: 5-year volatility marginally higher than 2-year German Bunds and lower than AA-rated corporate bonds.

The development of CLO ETFs represents a natural progression in market efficiency rather than an artificial attempt to provide retail access to private assets. These products leverage existing market infrastructure while adding the benefits of exchange-traded accessibility.

Traditionally, the CLO market was largely reserved for institutional investors such as banks and pension funds. Given the CLO market’s growing size and efficient trading, more open-ended funds have offered exposure to CLOs in recent years. Today, investment is now possible through ETFs, allowing additional market participants to gain access to the CLO market.

Conclusion

As the investment industry debates retail access to private markets, it's crucial to distinguish between truly private assets and established institutional markets like CLOs. The CLO market's public trading infrastructure, price transparency, and institutional framework make it fundamentally different from private markets.

CLO ETFs represent not a forcing of private assets into liquid structures but rather an efficient way to access an established, liquid market through familiar investment vehicles.

Endnotes

- City Velocity as at 31-Dec-24.

- Estimate based on Fair Oaks Capital’s discussions with multiple dealing desks.

- Citi Velocity as at 31-Dec-24.

- Fair Oaks Capital, Bank of America and Citi as at 27-Dec-24. BWIC data from Bank of America. US risk-retention compliant CLOs based on historical BWIC volumes from Citi. Includes an estimation for bilateral dealing. Average over trailing 3-year period.

- Fair Oaks Capital and JP Morgan as at 29-Nov-24. Euro CLOIE AAA Index return, Corporate 3-5 year index level. Sovereign 2Y total return calculated using mid yield and average duration over the period.

- Barclays Research, “CLOs: Global Ownership Update”, 25-Oct-24.